Oakmark International Fund – Investor Class

Average Annual Total Returns 03/31/23

Since Inception 09/30/92 8.69%

10-year 5.04%

5-year 1.46%

1-year 5.22%

3-month 13.91%

Expense Ratio: 1.04%

Expense ratios are from the Fund’s most recent prospectus dated January 28, 2023; actual expenses may vary.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. The investment return and principal value vary so that an investor’s shares when redeemed may be worth more or less than the original cost. The To obtain the most recent month-end performance data, view it here.

Fellow Shareholders,

The International Funds had a strong quarter both in absolute and relative returns. The Oakmark International Fund had a notable return of 13.9%, which added to its strong fourth quarter of 2022 performance of over 20%. This positive result was driven mostly by a rebound in our European holdings, especially those based in Germany. Note in our third-quarter 2022 commentary that we discussed “The Case for European Equities.” Though it is pleasing to see a rebound in European share prices, it should be noted that they still sell at measurable discounts compared to share prices in the rest of the world.

Bank or Banking System Crisis?

With the events surrounding Silicon Valley Bank (SVB), March saw prices of banks severely negatively impacted globally. In fact, even blue-chip banks, like BNP Paribas, were down as much as 25% in March before they slightly recovered. We feel this price reaction was overdone and not at all consistent with business fundamentals, as the global banking system has changed materially since the global financial crisis (GFC) when banks were far less capitalized and the quality of the assets they held were often poor. Following the crisis in 2008, new regulations were enacted that required banks to significantly grow their reserves and capital bases. As a result, lending and shareholder returns were muted and valuations were generally low, but the system became stronger.

The recent stress in the banking sector, highlighted by the collapse of SVB and Signature Bank, can be largely attributed to poor risk management at the affected institutions. There was a significant mismatch with the duration of their deposits (short term) and assets (long term). In addition, SVB had explosive growth in deposits with a high percentage of those above the FDIC insurance level that came from a non-diversified client base with concentrated exposure to niche industries, like venture capital and cryptocurrency. When these industries contracted significantly after the pandemic-induced boom, it resulted in a decline in deposits and a difficulty for the banks to honor withdrawals without realizing heavy losses on their high-quality but long-dated investments, which culminated with solvency fears and a run on the bank. Please see Bill’s commentary for more on this.

In contrast, our European bank holdings have securities portfolios that are much smaller as a percentage of assets than their U.S. counterparts. This results in our select European bank holdings having significantly less potential for unrealized losses in their securities portfolios than their U.S. peers. In fact, marking to market the securities portfolios of our European bank holdings would have an immaterial impact on their net worth and regulatory capital. Moreover, our European bank holdings possess strong and diversified deposit bases that should benefit from a flight to quality during periods of uncertainty.

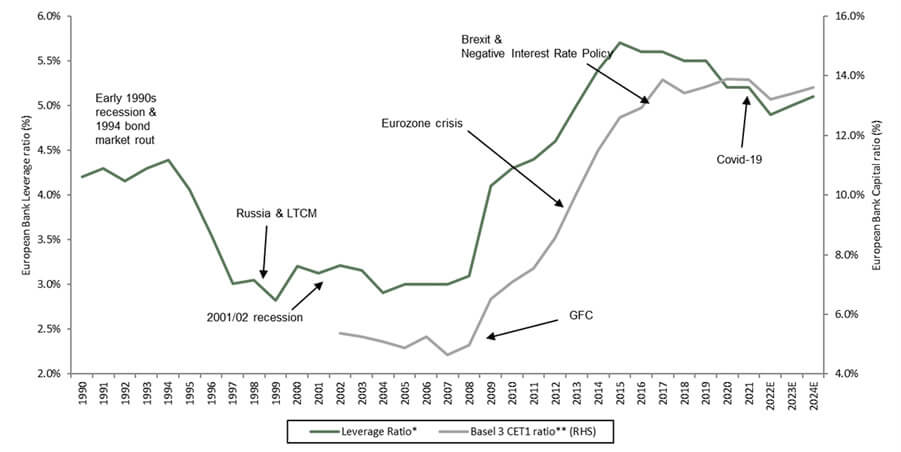

Furthermore, given banks now have higher amounts of capital on their balance sheets (see chart below) and higher quality assets, we believe they are poised to benefit from what we view as a triple positive: interest rate spreads increasing, resilient economies, and the ability to use earnings to grow their businesses or return capital to shareholders. Some of the highest quality banks we own, such as Intesa Sanpaolo, Lloyds Banking Group and BNP Paribas, are trading at low price-to-book and price-to-earnings ratios with high-dividend yields, 10%+ free cash flow yields, and excess capital to use toward increasing dividends or buying back stock. In the case of BNP Paribas, it sold Bank of the West in January for $16 billion, or 1.75-times book value, and it can use proceeds to repurchase its own shares at around half of book value, which is very value accretive.

Source: Bernstein Autonomous LLP. * Tangible equity/adjusted assets. ** Estimated prior to 2011 based off Basel 1 and Basel 2 ratios.

In summation, while certain banks are or were in crisis, we believe the banking system itself is not in crisis. Instead, we think banks provide opportunity for disciplined and patient investors.

Finally, An End to Our Investment in Credit Suisse

We were shareholders in Credit Suisse for more than two decades. We sold down much of our position prior to the GFC after the share price appreciated significantly and then rebuilt the position after the GFC. The second holding period was troubled and full of controversy as Credit Suisse’s investment bank experienced repeated lapses in risk management concurrent with its attempts to compete with more scaled peers. Despite this, we, in hindsight, incorrectly remained focused on our sum-of-the-parts valuation and gained comfort in the strong performance of its wealth management, asset management and Swiss Universal Bank businesses as they continued to generate better than average returns. We believed that the three better businesses represented good value and that the investment bank was repairable. Despite numerous attempts by multiple leadership teams at Credit Suisse, our thesis was proven wrong. Finally, after the last investment banking restructuring plan and capital raise released last October, we determined it was time to reevaluate our investment thesis as we do whenever there is a fundamental change in one of our holdings. The release of the plan provided us with NO insight into the proceeds from the asset sales as well as the costs of restructuring the investment bank. As such, we concluded that an accurate business valuation was indeterminable and compounded by inevitable years of cash outflows. In addition, Credit Suisse’s key wealth management franchise experienced elevated client withdrawals and risks of reputational damage to its wealth franchise brand grew. As such, we made the decision to exit our position in the fall of 2022 and completed our exit in early March of this year.

Investment Opportunity in Volatility

We find the presence of volatility usually widens the discrepancy between share price and the underlying intrinsic value of a business. As a fundamentally driven value investment manager, it presents us with the opportunity to advantageously position portfolios to maximize long-term return potential as demonstrated by what occurred in March within the global financials sector. If the share price of a high-quality business decreases sharply without a corresponding decline in our estimated intrinsic value, we use that as an opportunity to add to the position. As share prices converge with our perception of business value, we reduce position size. In previous times of crises, we adhered to our disciplined and time-tested investment process–and we will continue to do so.

Thank you for your continued support.

The securities mentioned above comprise the following preliminary percentages of the Oakmark International Fund’s total net assets as of 03/31/2023: Bank of the West 0%, BNP Paribas 3.0%, Credit Suisse 0%, Intesa Sanpaolo 2.9%, Lloyds Banking Group 2.8%, Signature Bank of New York 0% and Silicon Valley Bank 0%. Portfolio holdings are subject to change without notice and are not intended as recommendations of individual stocks.

Access the full list of holdings for the Oakmark International Fund here.

The securities mentioned above comprise the following preliminary percentages of the Oakmark International Small Cap Fund’s total net assets as of 03/31/2023: Bank of the West 0%, BNP Paribas 0%, Credit Suisse 0%, Intesa Sanpaolo 0%, Lloyds Banking Group 0%, Signature Bank of New York 0% and Silicon Valley Bank 0%. Portfolio holdings are subject to change without notice and are not intended as recommendations of individual stocks.

Access the full list of holdings for the Oakmark International Small Cap Fund here.

Price to Book Ratio is a stock’s capitalization divided by its book value. The projected P/B ratio uses the forecast book value for next year and the stock’s price at the indicated date.

The price to earnings ratio (“P/E”) compares a company’s current share price to its per-share earnings. It may also be known as the “price multiple” or “earnings multiple”, and gives a general indication of how expensive or cheap a stock is. Investors should not base investment decisions on any single attribute or characteristic data point.

The funds’ portfolios tend to be invested in a relatively small number of stocks. As a result, the appreciation or depreciation of any one security held by the Fund will have a greater impact on the Funds’ net asset value than it would if the Fund invested in a larger number of securities. Although that strategy has the potential to generate attractive returns over time, it also increases the Funds’ volatility.

The stocks of smaller companies often involve more risk than the stocks of larger companies. Stocks of small companies tend to be more volatile and have a smaller public market than stocks of larger companies. Small companies may have a shorter history of operations than larger companies, may not have as great an ability to raise additional capital and may have a less diversified product line, making them more susceptible to market pressure.

Investing in foreign securities presents risks that in some ways may be greater than U.S. investments. Those risks include: currency fluctuation; different regulation, accounting standards, trading practices and levels of available information; generally higher transaction costs; and political risks.

The information, data, analyses, and opinions presented herein (including current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) are for informational purposes only and represent the investments and views of the portfolio managers and Harris Associates L.P. as of the date written and are subject to change and may change based on market and other conditions and without notice. This content is not a recommendation of or an offer to buy or sell a security and is not warranted to be correct, complete or accurate.

Certain comments herein are based on current expectations and are considered “forward-looking statements”. These forward looking statements reflect assumptions and analyses made by the portfolio managers and Harris Associates L.P. based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Actual future results are subject to a number of investment and other risks and may prove to be different from expectations. Readers are cautioned not to place undue reliance on the forward-looking statements.

All information provided is as of 03/31/2023 unless otherwise specified.