Oakmark International Fund

Average Annual Total Returns 9/30/12

10-year 10.75%

5-year -0.11%

1-year 17.40%

Expense Ratio as of 9/30/11 was 1.06%

Oakmark International Small Cap Fund

Average Annual Total Returns 9/30/12

10-year 12.34%

5-year -1.87%

1-year 13.15%

Expense Ratio as of 9/30/11 was 1.38%

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. The investment return and principal value vary so that an investor’s shares when redeemed may be worth more or less than the original cost. The performance of the Funds does not reflect the 2% redemption fee imposed on shares redeemed within 90 days of purchase. To obtain the most recent month-end performance data, view it here.

Fellow Shareholders,

The Oakmark International and International Small Cap Funds recorded one-year returns of 17% and 13%, respectively, despite the fact that over the last year, the world experienced a heavy dose of economic and market uncertainty. This period marked a deepening macroeconomic and banking crisis in Europe, slower growth in the BRICS (Brazil, Russia, India, China and South Africa), and a Japanese economy is still struggling after the March 2011 earthquake and Thai floods later that year. Nevertheless, we are pleased with the absolute returns of both Funds over the last year. Though, on a relative basis, Oakmark International has been a bit more competitive versus its benchmark than Oakmark International Small Cap. (Please refer to separate Fund letters.)

Happy 20th Birthday, Oakmark International!

I personally celebrated 20 rewarding years at Harris Associates L.P. this August, and September’s end of 1992 marked the Oakmark International Fund’s inception. My early days at Harris Associates began

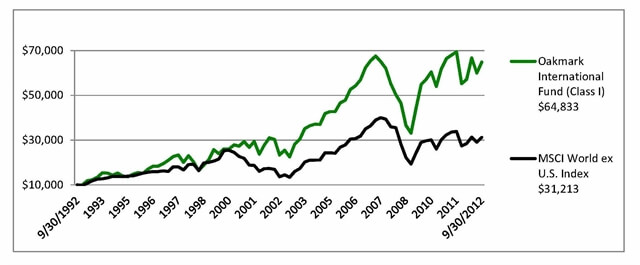

with a team of one (yours truly). With the addition of Mike Welsh shortly thereafter, a team slowly developed. Mike eventually became the first co-manager and, a bit after Mike’s retirement, Rob Taylor, our director of international research, joined me as the Fund’s second co-manager. We currently have nine analysts (including the portfolio managers, who are still involved in the analytical process) researching the investment ideas that go into the Fund. As a group, we believe that we have been successful for three reasons: First, we utilize a sound investment philosophy that defines our value-investing concept as one which notionally includes both low price and high quality; second, we execute this philosophy and approach in an extremely disciplined manner; and third, we have a group of investment professionals that not only improve over time but truly work as a team. We can proudly say that over the last 20 years, the Oakmark International Fund has indeed added value to those who have entrusted us with their savings by returning an average of 10% per year versus the MSCI World ex U.S. Index and the MSCI EAFE Index, which have returned an average of 6% per year.

One last ingredient to investment success is the importance of learning from mistakes. I have been in this industry for over 26 years, and I can say the one thing that does not change is the ill feeling I get when an investment idea doesn’t work. Mistakes become indelible in your mind, whereas success seems a bit fleeting. Perhaps this is the way it should be. I believe that mistakes can and should be a means to achieving better future performance if the particular mistake leads to a valuable lesson learned. What a mistake should not do is cause an “overcorrection” which ultimately will lead to more mistakes.

The Future

The beauty of this business is that there is really never a dull moment. Every few years, “stormy” market conditions appear that eventually end up leading to investment opportunities. The reason I believe we at Harris Associates are successful at “harvesting fear” is because we stubbornly make decisions based on company fundamentals rather than macroeconomic worries and market volatility. We don’t try to predict the Fed’s next move or on which cheek Hollande will kiss Merkel. We believe that investment success comes from correctly assessing business value, not from correctly predicting macro trends. We believe we will continue to make money for our shareholders and clients over the long term as long as we maintain three essential tenets: apply a disciplined and objective approach in valuating companies, buy low and sell high, and confidently act on our convictions. As simple as it sounds, that is in fact our “secret sauce.”

Here is to another solid 20 years for all of our shareholders. As always, your continued confidence is greatly appreciated.

The MSCI World ex U.S. Index (Net) is a free float-adjusted market capitalization index that is designed to measure international developed market equity performance, excluding the U.S. This benchmark calculates reinvested dividends net of withholding taxes using Luxembourg tax rates. This index is unmanaged and investors cannot invest directly in this index.

The MSCI EAFE Index is a stock market index that is designed to measure the equity market performance of developed markets outside of the U.S. & Canada. The index is market-capitalization weighted (meaning that the weight of securities is based on their respective market capitalizations). This index is unmanaged and investors cannot invest directly in this index.

Investing in foreign securities presents risks that in some ways may be greater than U.S. investments. Those risks include: currency fluctuation; different regulation, accounting standards, trading practices and levels of available information; generally higher transaction costs; and political risks.

The stocks of smaller companies often involve more risk than the stocks of larger companies. Stocks of small companies tend to be more volatile and have a smaller public market than stocks of larger companies. Small companies may have a shorter history of operations than larger companies, may not have as great an ability to raise additional capital and may have a less diversified product line, making them more susceptible to market pressure.The discussion of the Funds’ investments and investment strategy (including current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) represents the Funds’ investments and the views of the portfolio managers and Harris Associates L.P., the Funds’ investment adviser, at the time of this letter, and are subject to change without notice.