By Adam Abbas, Portfolio Manager

Key Takeaways:

- Today’s fixed income environment is marked by uncertainty, rising rates and concerns over short-term market variables.

- A closer look at real and nominal yields and viewing fixed income through a value investing lens may provide a different view from the consensus.

- Although the challenges exist, there are unique opportunities for value investors by pinpointing intrinsic value and harnessing rising yields.

Today’s environment poses distinct challenges in the short run, especially for investors anchored in value investing principles. Currently, the investment landscape is impacted by the effects of a Federal Reserve hike cycle initiated nearly two years ago, which was implemented to offset inflation. Yet, we are now in the midst of the most significant fixed income sell-off since the 1970s.

Fixed income – and the value proposition

Historically, fixed income assets have served as the bedrock of many investment portfolios. However, the current climate has stoked fear of the potential for additional major losses. Most conversations with anxious investors and the media now center around short-term market variables—oversupply, new bond issuance, interpretations of Federal Reserve guidance, and dot plots, to name a few. The shift away from fundamentals is noticeable.

Although fixed income’s immediate future might appear clouded, it’s important to note that Oakmark does not engage in near-term forecasting. Instead, we emphasize long-term value investing, and typically, when the investment community leans heavily into short-term concerns, opportunities in long-term value investing emerge.

So, let’s step back and evaluate the inherent value proposition of fixed income. Although most people associate value investing predominantly with stocks, it’s an equally crucial concept in bond investing. As Howard Marks wisely put it, investing intelligently is about determining an asset’s genuine value and securing it for less than that amount. This calls for a consistent approach, especially when temporary factors have created short-term price swings.

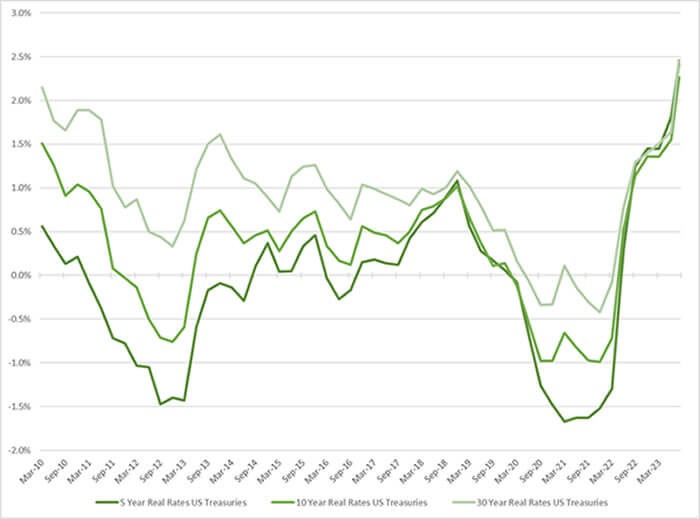

We believe that government and high-quality U.S. bonds have stronger long-term value now than they’ve exhibited in over a decade. Our view surely runs counter to natural instincts to sell and move to cash, especially given the rising rates and lower prices that continue week after week. Yet, the essence of value investing is acquiring assets at or below their true worth, ensuring a sizeable safety net. Real yields now offer that safety net. After averaging negative real returns over the previous decade, U.S. government bonds now guarantee over 2% annual real rates of returns beyond inflation forecasts for every spot on the duration curve (see Figure 1). High-quality corporations, which have historical default rates below 2%, are now providing over 4% yields to investors adjusted for inflation.

Figure 1: Real yields in U.S. Government Treasurys

What investors are compensated for over inflation expectations

Source: Bloomberg; U.S. Treasurys real rates, H15 index (5 year, 10 year, 30 year); dates depicted 3/31/2010 – 8/31/2023

Inflation: Don’t fight the Fed

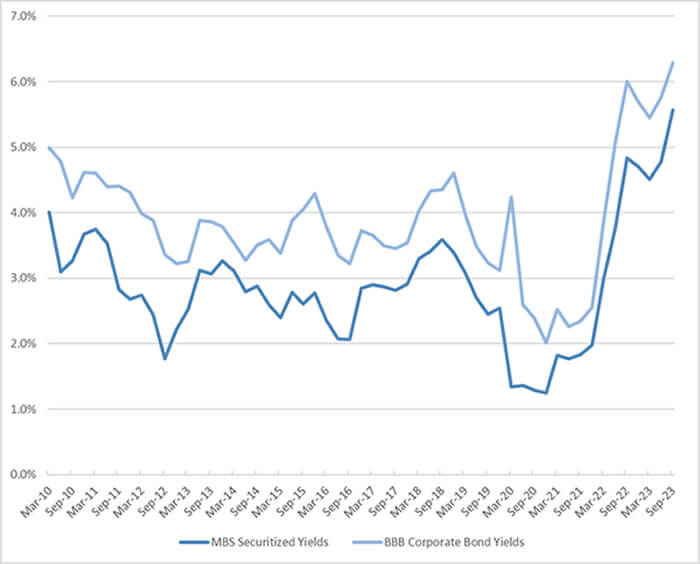

But the significant jump in value vis-a-vis both real and nominal yields (see Figure 2) is mostly being ignored. Instead, the focus seems to be on short-term phenomena like supply imbalances, technical trading levels, structural shifts in the labor markets, disruptions in the global supply chain, and even the largely theoretical discussions on the potential impacts of quantitative tightening (QT). There’s a clear fixation—almost a panic—about the risks of more inflation, and it dominates much of the discourse.

Figure 2: Nominal yields for high-quality fixed income

Yields are now significantly above the post global financial crisis highs

Source: Bloomberg; LUMSYW Index – Bid Price, LCB1YW Index – Last Price; dates depicted 3/31/2010 – 9/29/2023

However, despite the persistent “inflation-forever” discussions, it’s imperative to recognize the Federal Reserve’s unwavering commitment to its 2% inflation target. The well-known mantra, “Don’t fight the Fed,” is timely. Historically, even though the Federal Reserve might sometimes be delayed in its actions, it inevitably meets its objectives. Those challenging Chairman Jerome Powell’s stance on the 2% mandate might want to reconsider; past events reveal that doubting the Fed’s eventual victory often results in both one’s pride and one’s pocketbook taking a hit. Simply put, the Fed will achieve its mandate and either inflation will 1) continue to slow gradually, providing the Fed with a smooth transition (aka “soft landing”) or 2) buckle under prolonged restrictive monetary policies. When will this happen? It’s hard to pin down. Yet, a significant reduction in policy rates, as aligned with the Fed’s intentions, appears inevitable over the medium term one way or the other. If our assessment holds, long-term investors like Oakmark, who focus on the bigger picture rather than timing the market or chasing quarterly trends, have a wealth of opportunities in top-tier fixed income assets.

Driving income: Yield counts

Income, too, forms an indispensable part of the value proposition today. Yields have risen across the fixed income landscape, emphasizing that the value isn’t solely in potential price returns. Suppressed rates in the post-global financial crisis era have overshadowed this element, but its significance for fixed income’s value proposition should not be ignored. Higher yields inherently mean a margin of safety. There is a built-in cushion with these assets, and that cushion puts them in line with Oakmark’s core principles of value investing.

Take leveraged loans as an example. Due to the rate increases over the past two years, our top picks in the high-quality leveraged-loan category now offer yields ranging from 6.5% to 7.5%. We assess their default risk to be in line with many of our investment-grade corporate bonds that produce considerably less recurring income. Though callability caps their price appreciation potential, the steady income they generate in the current rate environment provides substantial intrinsic value.

In the face of a possible extended period of elevated interest rates, the dual pillars of capital appreciation and income will undeniably shape the value narrative for fixed income assets. Past lessons illuminate this dynamic. Reflecting on the bond bear market of the 1970s, those who steadfastly reinvested their income not only preserved their capital but saw it substantially grow by the time Volker initiated his anti-inflation measures—a vivid testament to the enduring power of compounding and reinvested interest, even amid ascending yields.

Though fraught with challenges, the current fixed income landscape unveils unique opportunities for astute investors who are committed to value principles. Amid the cacophony of short-term concerns and the specter of inflation, the true north of value investing endures: pinpointing intrinsic value and harnessing the sustained might of income. As yields ascend and real rates bolster the safety net, bonds emerge not merely as tools for hedging or dampening volatility, but as arenas ripe for genuine value discovery.

OPINION PIECE. PLEASE SEE ENDNOTES FOR IMPORTANT DISCLOSURES.

The information, data, analyses, and opinions presented herein (including current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) are for informational purposes only and represent the investments and views of the portfolio managers and Harris Associates L.P. as of the date written and are subject to change and may change based on market and other conditions and without notice. This content is not a recommendation of or an offer to buy or sell a security and is not warranted to be correct, complete or accurate.

Certain comments herein are based on current expectations and are considered “forward-looking statements.” These forward looking statements reflect assumptions and analyses made by the portfolio managers and Harris Associates L.P. based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Actual future results are subject to a number of investment and other risks and may prove to be different from expectations. Readers are cautioned not to place undue reliance on the forward-looking statements.

GFC refers to the global financial crisis of 2008.

The Oakmark Bond Fund invests primarily in a diversified portfolio of bonds and other fixed-income securities. These include, but are not limited to, investment grade corporate bonds; U.S. or non-U.S.-government and government-related obligations (such as, U.S. Treasury securities); below investment-grade corporate bonds; agency mortgage backed-securities; commercial mortgage- and asset-backed securities; senior loans (such as, leveraged loans, bank loans, covenant lite loans, and/or floating rate loans); assignments; restricted securities (e.g., Rule 144A securities); and other fixed and floating rate instruments. The Fund may invest up to 20% of its assets in equity securities, such as common stocks and preferred stocks. The Fund may also hold cash or short-term debt securities from time to time and for temporary defensive purposes.

Under normal market conditions, the Fund invests at least 25% of its assets in investment-grade fixed-income securities and may invest up to 35% of its assets in below investment-grade fixed-income securities (commonly known as “high-yield” or “junk bonds”).

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments.

Bond values fluctuate in price so the value of your investment can go down depending on market conditions.

All information provided is as of 09/30/2023 unless otherwise specified.