Oakmark Bond Fund – Institutional Class

Average Annual Total Returns 03/31/21

Since Inception 06/10/20 3.77%

3-month -1.08%

Gross Expense Ratio: 2.82%

Net Expense Ratio: 0.59%

Expense ratios are based on estimated amounts for the current fiscal year; actual expenses may vary.

The Fund’s Adviser has contractually undertaken to waive and/or reimburse certain fees and expenses so that the total annual operating expenses of each class are limited to 0.64%, 0.59%, and 0.44% of average net assets, respectively. The contractual advisory fee waiver agreement is effective through January 27, 2022.

Past performance is no guarantee of future results. The performance data quoted represents past performance. Current performance may be lower or higher than the performance data quoted. The investment return and principal value vary so that an investor’s shares when redeemed may be worth more or less than the original cost. To obtain the most recent month-end performance data, view it here.

The prevailing sentiment surrounding rates is scary stuff. The most common threads read like a collection of nightmares from the Fed’s past: stark warnings of runaway inflation, taper tantrums and lost credibility are the most popular. Low-probability events like these can cause large problems across financial markets, but it’s important to frame the current risks properly. We are skeptical that all of today’s prognosticators have investors’ best interests at heart. Instead, many are driven by ratings, clicks, views, likes and retweets. And in a world where competition for attention grows every day, you better project something riveting if you want to get noticed, even if your prediction isn’t very likely. In this environment, compelling doomsday forecasts proliferate, while far more likely scenarios receive much less coverage than they should. So, in Oakmark fashion, we’ll take this opportunity to offer a counterbalance to the fever-pitch analysis that’s dominating today’s news and make some more measured comments on rates and inflation.

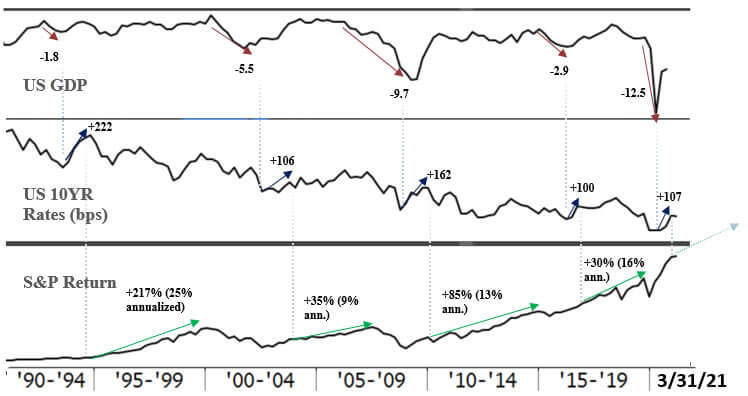

Rates are doing exactly what one would hope at the beginning of a sustainable recovery. As painful as the rate moves have been for bond returns, nothing about the degree of the rate rise has been unusual. In fact, since 1990, every meaningful U.S. economic contraction (defined by a GDP contraction of >1.5%) has been quickly followed by large, short bursts in rates. Specifically, following the four most recent recessionary periods prior to 2020, the U.S. 10-year Treasury rates rose an average of about 150 basis points within the first four quarters of the expansion. [See Table 1.] Today, four quarters after the Covid-19-related sudden stop to the economy, the magnitude of the current 10-year upswing falls short of the average, reaching 107 basis points. What’s more, previous jumps in rates like this have not derailed the markets. In fact, it’s been quite the contrary. In the three to five years following such increases, most major asset classes, including investment grade credit, high yield credit and equities, to name a few, have experienced above-average returns.

Table 1: Large bursts in 10-year U.S. rates are normal after periods of economic contraction and have preceded strong periods of market returns.

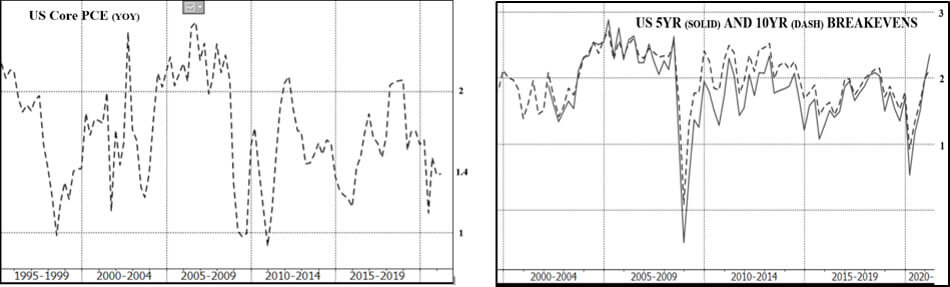

And inflationary risks might be overblown. Today, we hear a lot about how we may be approaching the same kind of runaway inflation experienced in the 1970s. The basic thesis is that unprecedented amounts of both monetary and fiscal stimulus, combined with a more reactionary approach to monetary policy by the Fed, will eventually undermine the central bank’s ability to anchor expectations, causing prices to increase uncontrollably. Yet, if we’ve learned anything from the past two decades, it’s that major structural differences in the modern economy and a vastly more intelligent central banking system have produced much shorter inflationary periods. Current data continue to indicate that inflationary risks are limited and recent fears about inflation are more rooted in fear than in reality. For example, today, the U.S. core PCE is approximately 1.4%; Europe, Japan and Chinese core runs even weaker at 1%, 0.3% and 0%, respectively. U.S. breakevens tell a similarly benign story, stalling out despite several significant catalysts, including a new multi-trillion infrastructure plan, positive reopening news and very strong employment reports. Sure, prices will likely spike across several categories as we move into summer, but inflation does not get out of control due to isolated, temporary spikes over a few months. Instead, it requires sustained upward price pressure over multiple quarters, if not years. It must be long enough to embed a fundamental, widespread change in marketplace psychology.

A lift in yields at the beginning of a recovery should be welcomed, not feared. Rates are a friend, not foe, when they reflect a positive inflection in the potential real growth of an economy and prices are relatively well-anchored. Of course, increasing rates during an economic recovery will inevitably cause some volatility and disruption. We should expect more of these periods over the coming quarters, though we expect they will be brief. When they occur, it will be critical to lean on the data, rather than emotional reactions, to evaluate the risk. Talk of hyper-inflationary risk appears to only be growing louder and alarms have been sounded time and time again over the past two decades only to leave investors disappointed. It may serve as a less catchy story, but we think they could be disappointed again.

Performance and Outlook

The Oakmark Bond Fund returned -1.08% year to date through March 31, 2021, and generated 229 basis points of excess returns versus its benchmark, the Bloomberg Barclays U.S. Aggregate Index. Inception-to-date performance was 3.77% through March 31, 2021, generating excess return against the benchmark of 548 basis points.

The Fund’s outperformance continues to be driven by the portfolio’s overweight allocation to corporate credit, our short curve positioning and security selection. Specifically, during the quarter, our corporate ownership averaged 58% compared to the benchmark average of 28%. Recent credit spread tightening especially helped our corporate holdings. We maintain shorter curve positioning because we continue to believe that rates will increase. At the end of the quarter, the duration in the portfolio was a full 1.0 years below the benchmark, averaging 5.4 years, compared to the benchmark’s 6.4 year average duration. The last main contributor to the Fund’s outperformance came from security selection, including Chesapeake Energy, Broadcom Inc. 3.5 2/15/41 and Range Resources 8.25 1/15/29. We remain conservative about security quality. Currently, about 10% of the Fund’s corporate holdings are “A” rated credit or higher, 25% are “BBB,” 18% of corporates in BB, and just 4% of the overall portfolio in B or below rated credit. We are also underweight in volatile sectors, like basic materials and energy. During the quarter, we decreased our exposure to lower rated credit as spreads contracted and portfolio duration was modestly increased when yields increased.

Outlook and Positioning

Despite a rather dramatic backdrop for fixed income in the first quarter, we ended the period with a consistent approach to positioning. We maintained an overweight position in corporate credit risk, an underweight position in duration and a modest overweight to the short end of the yield curve. Looking forward, we believe corporate credit should perform well—especially relative to rates—and we expect growing economic tailwinds to maintain downward pressure on corporate default risk. As we highlighted in our opening commentary, we think that even as rates return to more normal levels, they can continue to support healthy markets and we believe that the risks of central banks losing control remain low. That being said, there are several risks that warrant careful observation in the second quarter. We will continue to monitor key price metrics heading into the summer, especially to make sure that rate spikes are absorbed and inflation expectations remain relatively well anchored at just above 2%. Also, Fed tapering will likely become more topical, so we will carefully examine even the slightest changes in Powell’s positioning. At the company level, capital structures now offer little in the way of covenant protection and wide-open capital markets are allowing fundamentally challenged companies to access debt markets. Because of these significant risks, our focus on bottom-up research remains critical.

The securities mentioned above comprise the following percentages of the Oakmark Bond Fund’s total net assets as of 03/31/21: Broadcom Inc. 3.5 2/15/41 0.0%, Chesapeake Energy 0.0% and Range Resources 8.25 1/15/29 0.0%. Portfolio holdings are subject to change without notice and are not intended as recommendations of individual stocks.

Access the full list of holdings for the Oakmark Bond Fund as of the most recent quarter-end.

The “core” PCE price index is defined as personal consumption expenditures (PCE) prices excluding food and energy prices. The core PCE price index measures the prices paid by consumers for goods and services without the volatility caused by movements in food and energy prices to reveal underlying inflation trends.

The Oakmark Bond Fund invests primarily in a diversified portfolio of bonds and other fixed-income securities. These include, but are not limited to, investment grade corporate bonds; U.S. or non-U.S.-government and government-related obligations (such as, U.S. treasury securities); below investment-grade corporate bonds; agency mortgage backed-securities; commercial mortgage- and asset-backed securities; senior loans (such as, leveraged loans, bank loans, covenant lite loans, and/or floating rate loans); assignments; restricted securities (e.g., Rule 144A securities); and other fixed and floating rate instruments. The Fund may invest up to 20% of its assets in equity securities, such as common stocks and preferred stocks. The Fund may also hold cash or short-term debt securities from time to time and for temporary defensive purposes.

New Fund Risk: The Fund is recently established and has limited operating history. The Fund may not be successful in implementing its investment strategy.

Under normal market conditions, the Fund invests at least 25% of its assets in investment-grade fixed-income securities and may invest up to 35% of its assets in below investment-grade fixed-income securities (commonly known as “high-yield” or “junk bonds”).

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments.

Bond values fluctuate in price so the value of your investment can go down depending on market conditions.

The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, mortgage-backed securities (agency fixed-rate and hybrid ARM pass-throughs), asset-backed securities and commercial mortgage-backed securities (agency and non-agency). This index is unmanaged and investors cannot invest directly in this index.

The information, data, analyses, and opinions presented herein (including current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) are for informational purposes only and represent the investments and views of the portfolio managers and Harris Associates L.P. as of the date written and are subject to change and may change based on market and other conditions and without notice. This content is not a recommendation of or an offer to buy or sell a security and is not warranted to be correct, complete or accurate.

Certain comments herein are based on current expectations and are considered “forward-looking statements”. These forward looking statements reflect assumptions and analyses made by the portfolio managers and Harris Associates L.P. based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Actual future results are subject to a number of investment and other risks and may prove to be different from expectations. Readers are cautioned not to place undue reliance on the forward-looking statements.

All information provided is as of 03/31/2021 unless otherwise specified.